Private AI for regulated banks: architecture before ambition

In banking, private AI is not a preference. It is a regulatory and governance requirement when AI affects credit, fraud, AML, risk, or regulated operations.

Why public AI is structurally weak for banks

SR 11-7 requires inventory, validation, documentation, monitoring, and governance for production models. DORA increases pressure around third-party ICT concentration risk. The EU AI Act requires documentation, testing, and oversight for high-risk uses. A bank cannot satisfy those duties with black-box AI it does not control.

What a viable architecture looks like

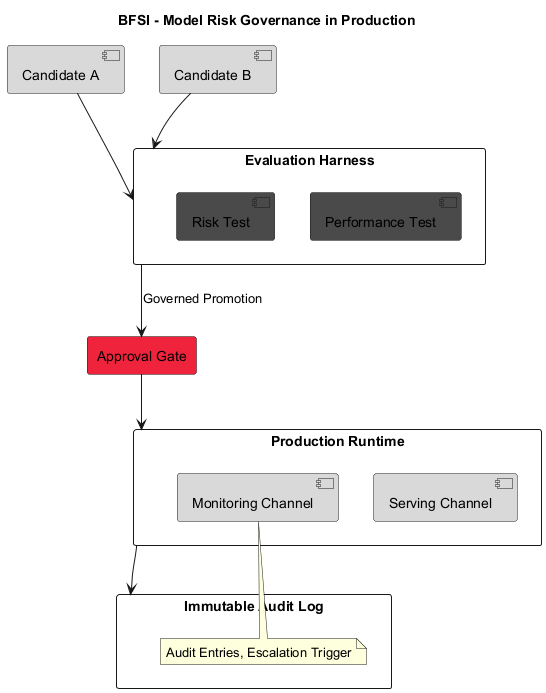

The deployer must own the model, logs, evaluation logic, and explanation artifacts. Real governance means model inventory, evidence trails, and independent validation capability inside the institution’s control boundary.

Where to start

Entry points with strong commercial logic include AML false positive reduction, fraud detection, AI banking assistants grounded on internal content, and document intelligence for high-volume operations.